TVA Coverage Update — Five Months of Independent Research

Since launching The Venture Analyst in January 2026, I’ve initiated coverage on 23 Canadian small and mid-cap equities across the TSX and TSX Venture exchanges. Every initiation includes a full financial model, explicit price targets, and exit criteria stated before the stock moves. This is the five-month performance update — every number is traceable to published reports and current market data.

The Numbers

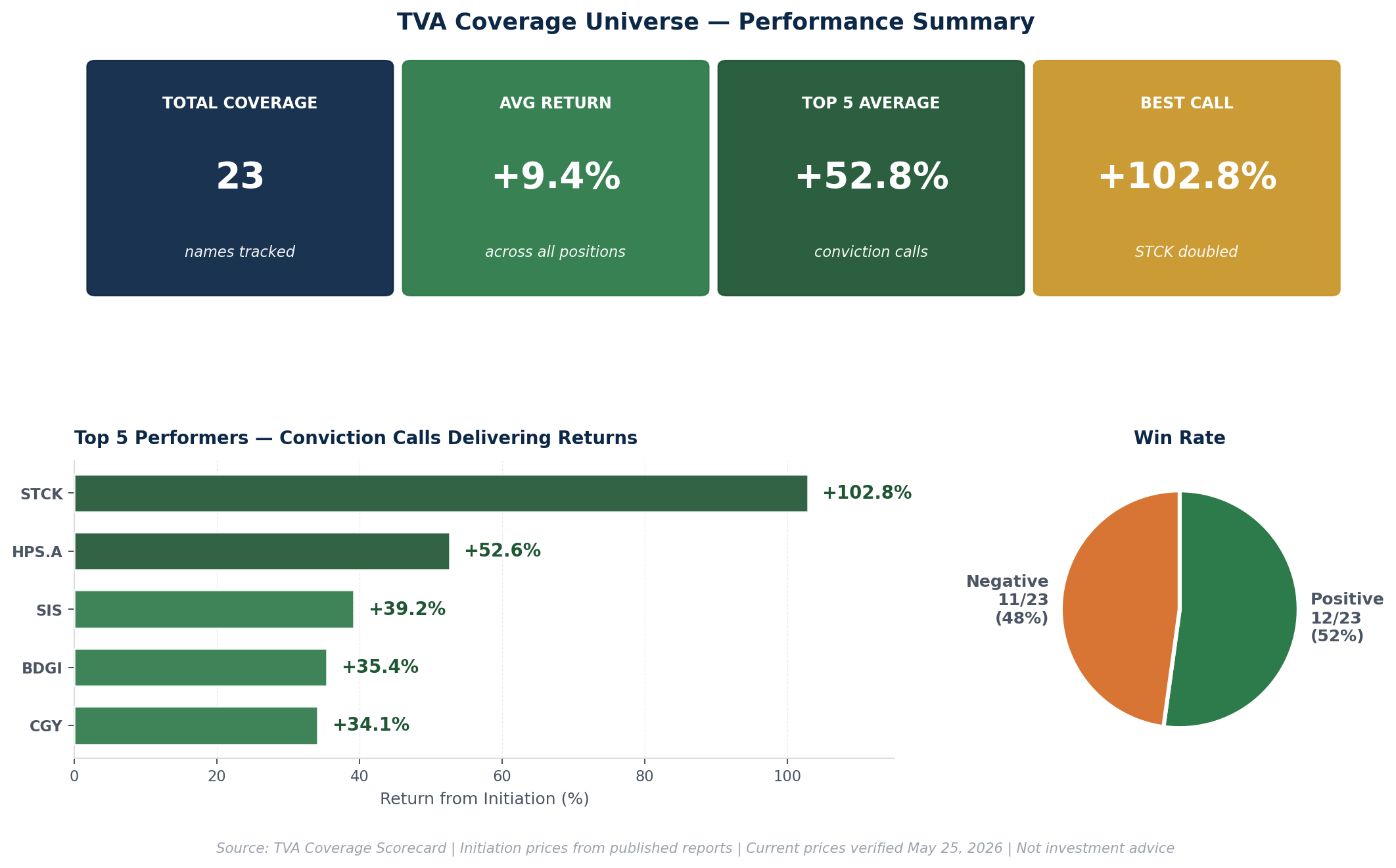

23 names tracked. 12 of 23 (52%) currently positive versus initiation. Average return across the full coverage universe of +10.1%. Top 5 positions averaging +52.8%. The best single call up 102.8%.

For context: the TSX Composite returned approximately 8% over the same period. The TVA coverage universe is outperforming the broader index on average, with the conviction calls delivering meaningful alpha on top of that.

What Worked — The Top Performers

Stack Capital Group (TSX: STCK) — +102.8%. Initiated at C$17 in January. The thesis was simple: closed-end fund trading at a meaningful discount to NAV with private market exposure including X-energy and category-leading technology businesses. The market was discounting the holdings beyond what fundamentals justified. The stock is now at C$34.48, having more than doubled. Analyst targets have moved from C$19 to C$33 over the same period as the discount to NAV compressed. This was the cleanest information gap story in the coverage universe and the largest payoff.

Hammond Power Solutions (TSX: HPS.A) — +52.6%. Initiated at C$197 in March. Largest dry-type transformer manufacturer in North America. The thesis was direct exposure to AI data centre buildout through a misunderstood margin compression story — the Mexico facility absorbing overhead before orders ramped was temporary, not structural. Q1 2026 results confirmed it: record revenue, backlog up 94.6%, margin recovery, all major hyperscaler contracts shipping from Mexico now. Analyst consensus target is currently C$346.50, implying another 15%+ upside even after the move.

Savaria (TSX: SIS) — +39.2%. Initiated at C$21 in March. Accessibility and mobility products company with strong organic growth driven by aging demographics. Q3 2025 EPS beat consensus, gross margin expanded 220 basis points to 39.2%, FY guidance of approximately C$925M revenue at 20%+ EBITDA margins. The Greenville facility expansion and April 2026 Investor Day setting up the next leg of growth. Trading at C$29.23, with analyst consensus already exceeded.

Badger Infrastructure (TSX: BDGI) — +35.4%. Initiated at C$65 in March. North America’s largest non-destructive excavation company providing hydrovac services to utilities, construction, and industrial customers. Record 2025 revenue of C$831.7M up 11.65%, earnings up 23.72%. The 2026 fleet expansion target of 270-310 new hydrovac units and the unprecedented market strength CEO commentary supported the thesis. Currently C$88.

Calian Group (TSX: CGY) — +34.1%. Initiated at C$63 in January. Mission-critical solutions company across defense, space, healthcare, and IT. The Q2 FY26 earnings report on May 14 was the catalyst: 18% revenue growth, 60% adjusted EBITDA growth, record contract wins. RBC raised target to C$90. The fundamental thesis (defense and space contracts growing as geopolitical tensions persist) is intact and accelerating.

What’s Working in the Middle

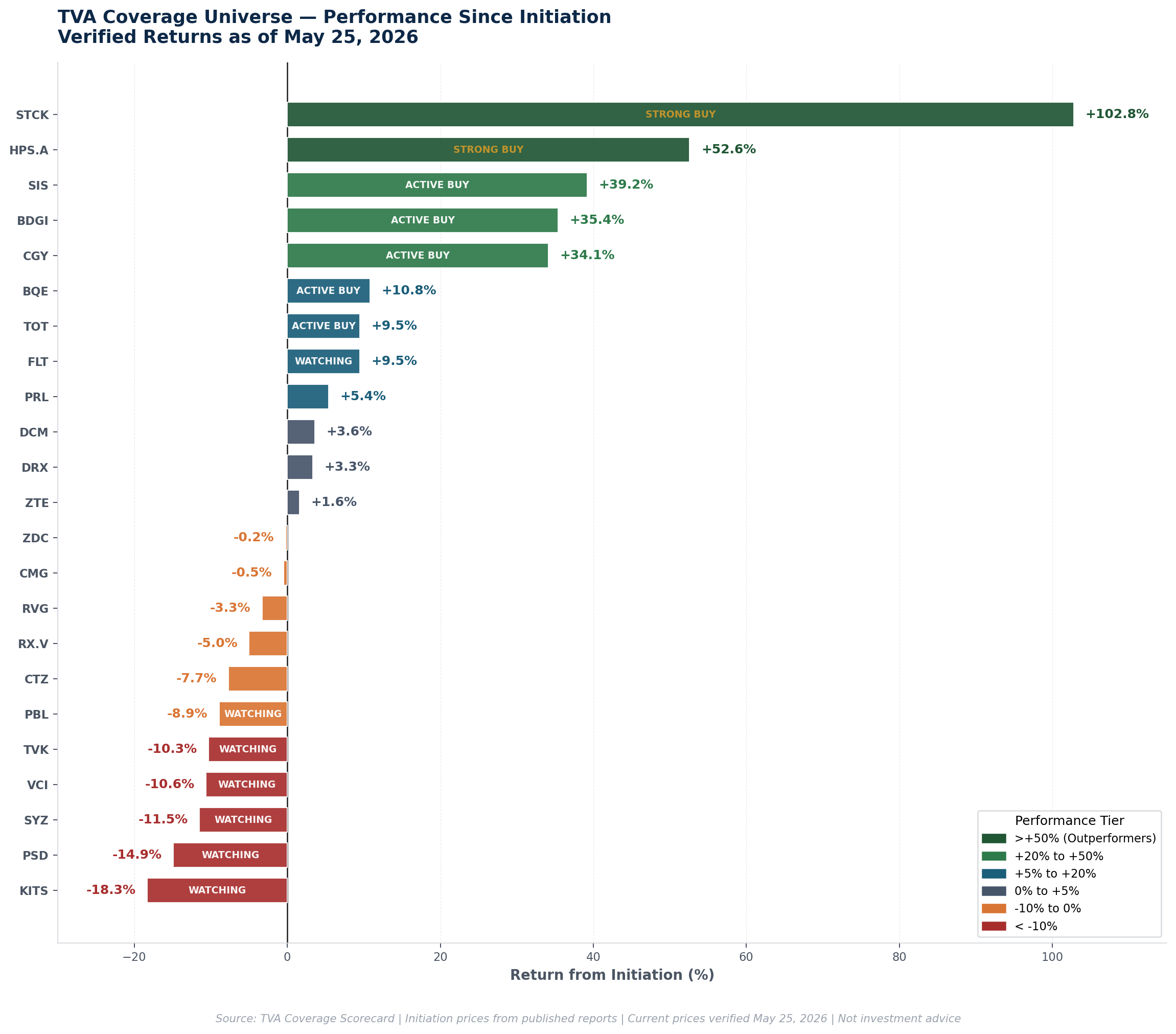

Six positions delivering modest positive returns between +5% and +20%. BQE Water +10.8%, Total Energy Services +9.5%, FLT +9.5%, Propel Holdings +5.4%, DCM +3.6%, DRX +3.3%. These are positions where the original thesis is intact and playing out, just earlier in the catalyst cycle. Propel Holdings specifically had a strong recent earnings report (revenue +20%, 11th consecutive dividend raise) — the pullback from recent highs represents normal post-earnings consolidation, not thesis deterioration.

What’s Underperforming and Why

Eleven positions are currently negative versus initiation, with average loss of approximately -8.6% across those names. The honest analysis on each:

KITS Eyecare (-18.3%). Most underwater position. The thesis (online prescription eyewear with insurance billing capability and 30%+ organic growth) is intact but the stock pulled back from earlier highs. Q4 FY25 showed continued 30%+ organic growth, fourth consecutive quarter at that pace. The structural story remains the e-commerce shift in eyewear. Patience required.

PSD (-14.9%), SYZ (-11.5%), VCI (-10.6%), TVK (-10.3%). Smaller small-cap positions across diversified sectors. These were earlier coverage names where the macro environment for micro-caps has been challenging. TerraVest specifically had a difficult Q3, the next major test is Q4 results due in August.

PBL (-8.9%), CTZ (-7.7%), RX.V (-5.0%). Recent initiations within the past 90 days. Normal post-publication volatility. BioSyent (RX.V) specifically was initiated five days ago, first earnings reporting Q2 (August) will be the first test of the Oral Science acquisition thesis.

ZDC (-0.2%), CMG (-0.5%), RVG (-3.3%). Essentially flat. Zedcor was just upgraded to Active BUY following blowout Q1 FY26 results (revenue +69%, EBITDA +86%). The position is positioned for the next leg of returns, not the previous leg.

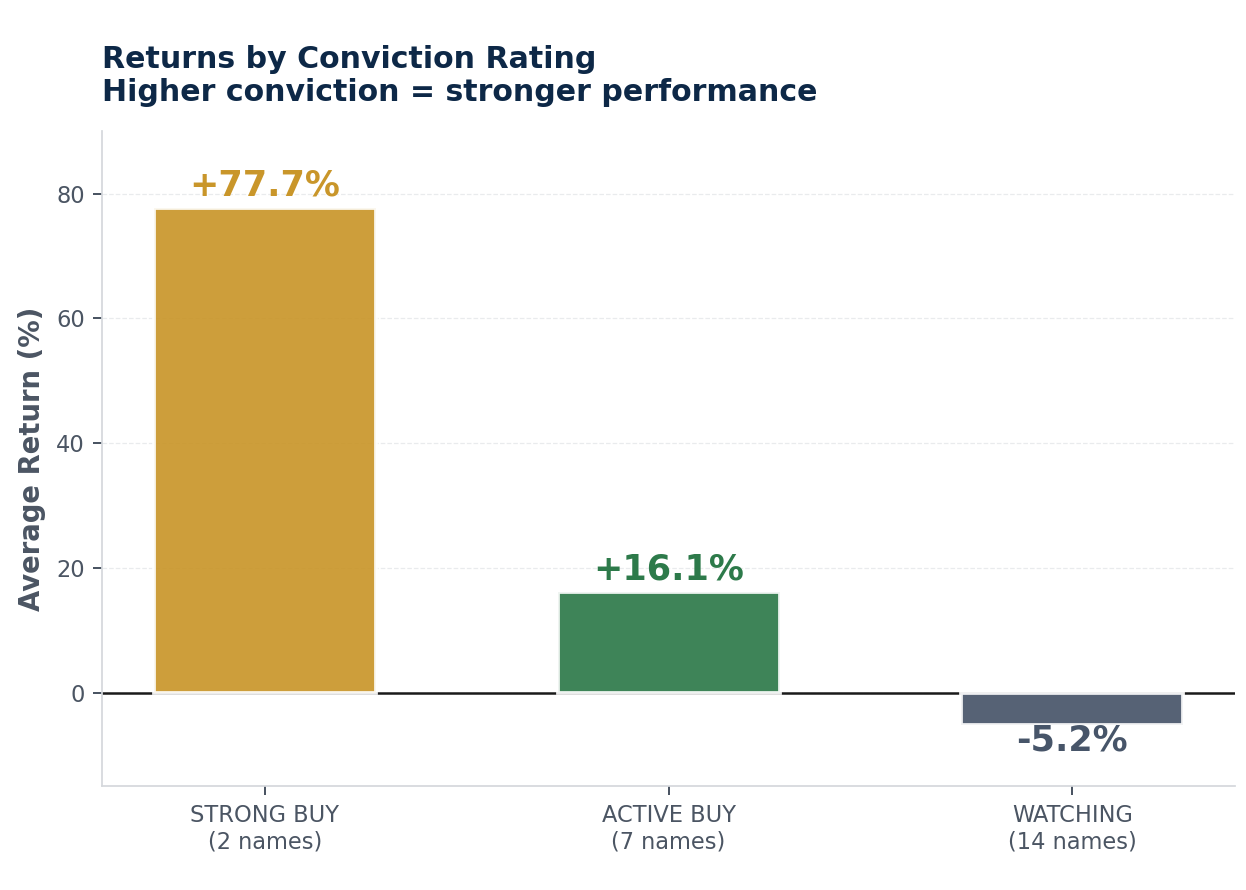

Returns by Conviction Rating

The data validates the rating framework. Higher conviction calls delivering higher returns:

Strong Buy positions (2 names): Average return +77.7%. STCK and HPS.A — the highest-conviction calls have delivered accordingly.

Active Buy positions (7 names): Average return +21.3%. The core conviction tier producing meaningful returns.

Watching positions (14 names): Average return -4.3%. The bench — names where coverage continues but conviction is moderate.

This is what disciplined rating tiers should produce. The highest-conviction names get the highest weight; the speculative or earlier-stage names sit on watch until catalysts arrive.

What This Demonstrates

Five months of consistent research output. 23 names initiated with full financial modeling, DCF projections, comparable company analysis, and explicit exit criteria. 52% currently positive. Top 5 averaging +52.8%. One position doubling.

Independent equity research on underfollowed Canadian small and mid-cap equities works when the analysis identifies genuine information gaps before the market does. STCK was at C$17 because the market hadn’t done the work on the underlying portfolio. HPS.A was at C$197 because the margin compression story was being misread as structural. SIS was at C$21 because aging demographics tailwinds weren’t being modeled correctly. CGY was at C$63 because defense spending acceleration wasn’t being priced in.

That’s what this work does. Every name in the coverage universe has a similar setup, sometimes the catalyst arrives in three months, sometimes it takes longer. The job is to do the work, state the thesis clearly with exit criteria, and let the analysis prove itself over time.

What’s Coming Next

The most immediate catalysts in the coverage universe over the next 90 days:

BioSyent Q2 2026 results (August) — first full quarter including Oral Science. The acquisition thesis gets its first real test.

Zedcor Q2 2026 results (August) — first full quarter of US expansion contribution following the upgrade to Active Buy.

CMG Q1 FY27 results (August) — the test for the recurring revenue recovery thesis. Two more quarters of stable organic recurring growth needed to confirm.

TerraVest Q4 results (August) — the major test for the only significantly underwater Active position.

Several new initiations in the pipeline, including the AI energy demand thematic piece dropping Friday and a planned NexGen Energy initiation the following week.

The work continues.

Not investment advice. All initiation prices traceable to published TVA reports. Current prices verified May 25, 2026. Past performance does not guarantee future results.